Morgan Stanley: Duke, other utilities ignoring profit opportunity by failing to decarbonize rapidly

As the cost of clean energy has plummeted, energy analysts have reported with increasing frequency that a transition by utilities from coal to less costly clean energy would save the nation’s electricity customers billions of dollars.

The latest, and perhaps more surprising, wave of reporting comes from Wall Street analysts, who now say that in addition to saving customers money, a rapid coal-to-clean energy transition would also be highly profitable for utilities’ investors.

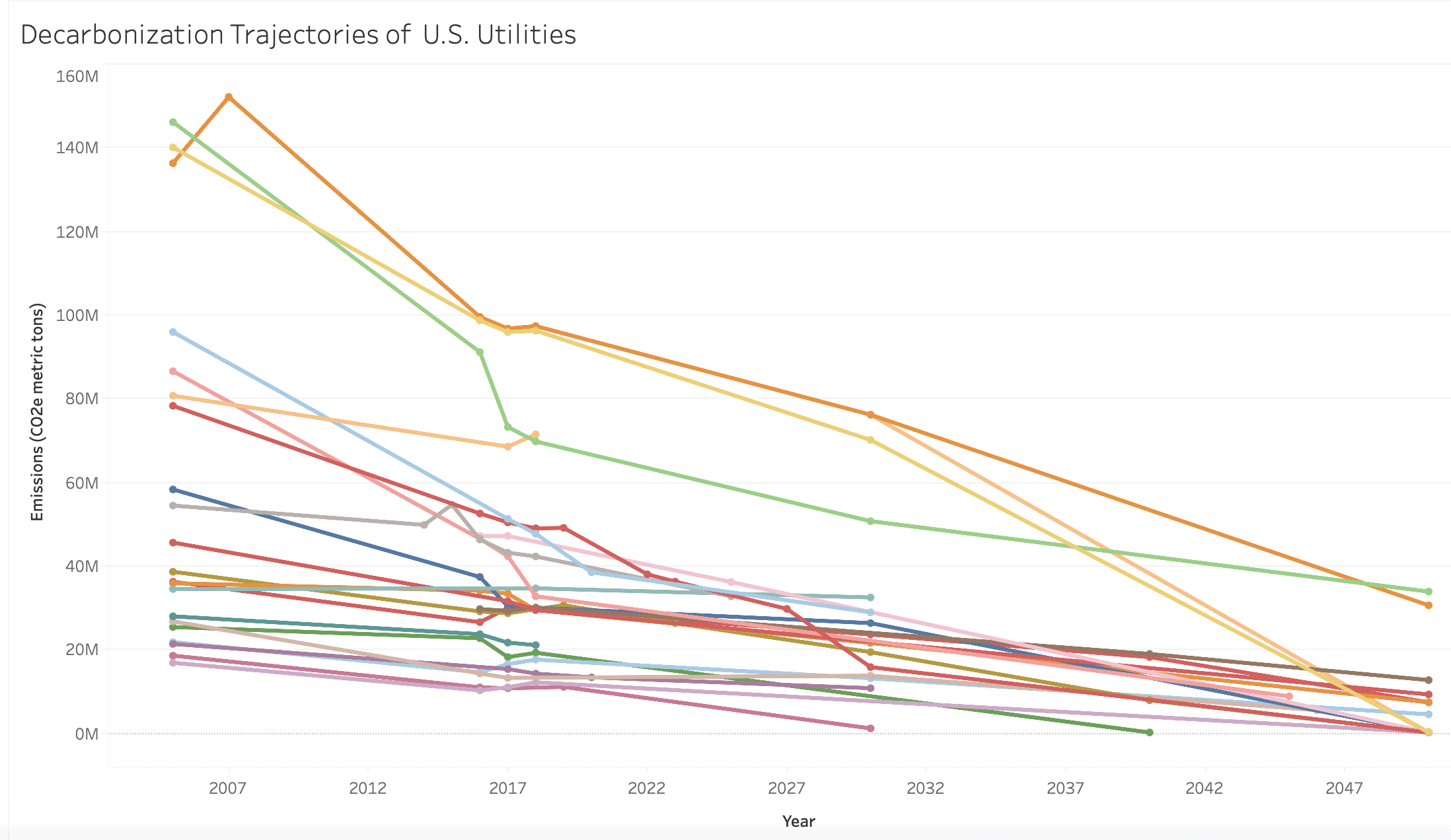

In a report released in late January, a team of analysts from Morgan Stanley led by Stephen Byrd analyzed the cost for 13 utilities of continuing to operate coal plants compared to retiring those assets and replacing them with renewable energy. Building on a previous report they released in December, the analysts found that the switch to lower-cost renewables creates an opportunity for the utilities to invest $64 billion in capital expenditures through 2025, creating profit opportunities while saving customers money.

But the analysts suggested that only some utilities are seizing that coal-to-clean profit opportunity, implying that others are eschewing potential earnings growth by keeping coal plants online and investing sluggishly in renewable energy.

Four key stocks – American Electric Power, Ameren, Duke Energy and Pinnacle West – had the greatest opportunity to profit from the coal-to-clean transition, according to the analysts. Of those, the analysts upgraded Ameren to “Overweight,” meaning they expect it to beat peers in the market, and they increased AEP’s price target.

The analysts said that while Duke Energy had the second-greatest earnings opportunity from the transition, they were only factoring that upside into Duke’s “bull” (or high upside) case.

“We are only including this upside in our bull case as the company has exhibited a slower than average pace in its decarbonization strategy,” the analysts wrote of Duke.

The analysts wrote the same message about three other stocks: FirstEnergy, PPL and Southern Co.

AEP and Ameren get stock boosts based on decarbonization opportunity

The Morgan Stanley report found that AEP stood to gain the most from decarbonization, with an earnings accretion potential of 14% by 2025. Based on an asset-by-asset analysis, the report found that 94% of AEP’s 124 GW of regulated coal plants will be rendered uneconomic by 2024, primarily by lower-cost wind energy. As a result, the analysts increased their price target for AEP by $8 per share, or 8% at the time of the report. Since the report release, Byrd upgraded AEP to “Overweight” alongside Ameren, saying that he prefers “exposure to low carbon intensity and decarbonization.”

The analysts found that of the 4.6 GW of coal that Ameren owns with no retirement date, roughly half will become uneconomic in Missouri by 2024, good for 6% earnings accretion by 2025. The analysts are waiting to see if the company converts those opportunities by accelerating its coal retirements and renewable energy investments when it files its next integrated resource plan in Missouri in September of this year.

Slow decarbonization paces for Duke, Southern, FirstEnergy mean lower earnings

The Morgan Stanley analysts’ characterization of Duke’s decarbonization pace as “slower than average” aligns with a flurry of other recent reports calling into question the integrity of Duke’s pledge to investors that it would be “net-zero” carbon by 2050.

Majority Action, which works with a coalition of institutional investors with $1.8 trillion of assets under management, released a report yesterday showing that Duke’s operating companies’ were acting out of alignment with the parent company’s climate goal.

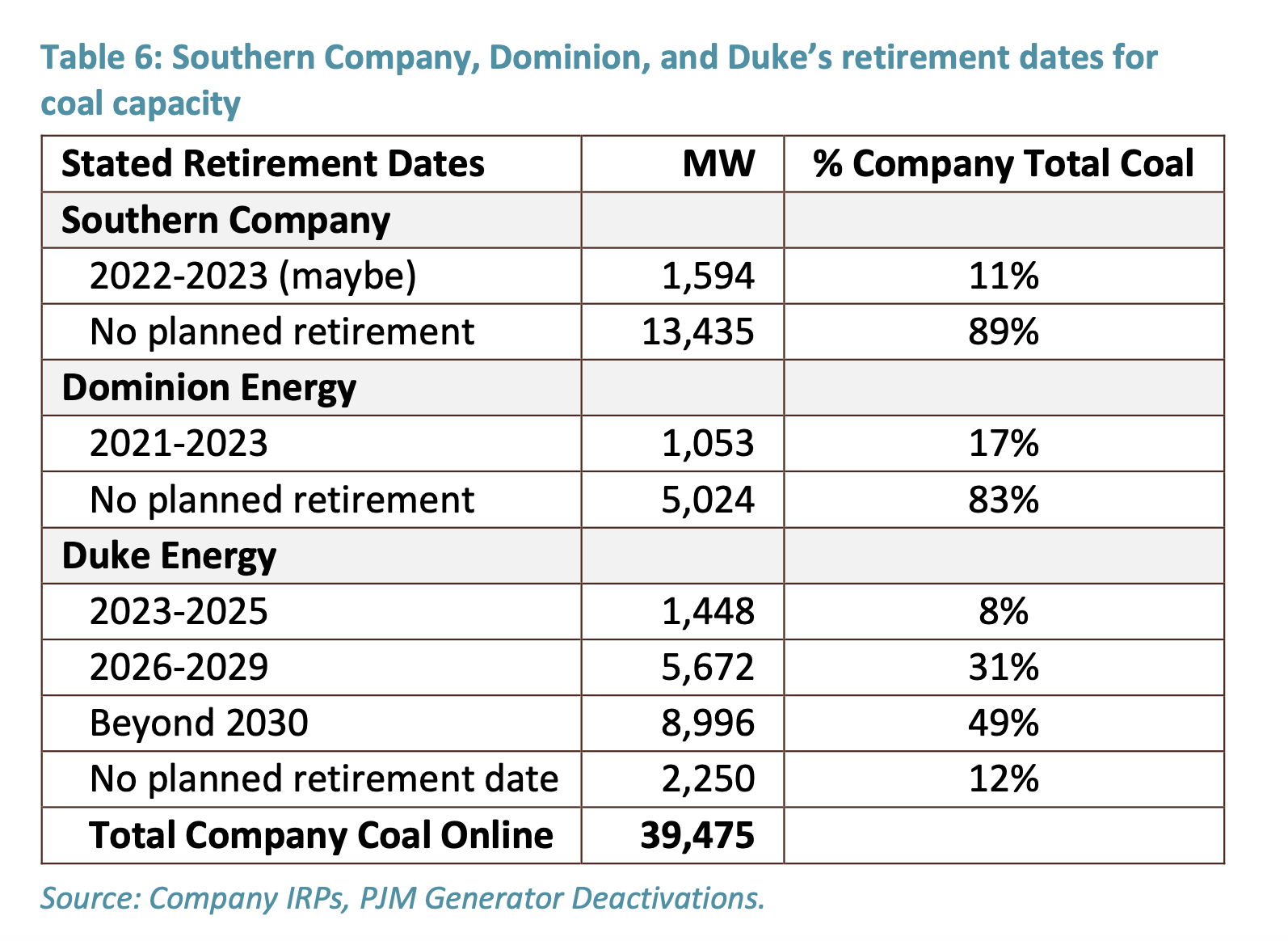

Duke is currently planning to keep 61% of its coal capacity online after 2030, the Majority Action report found. It has no retirement date at all for 12% of its coal capacity.

Southern Company has no planned retirement date for 89% of its coal capacity, the Majority Action report found.

To the extent both companies are retiring some coal plants, their current replacement plans have been dominated by gas, rather than clean energy.

Duke Energy’s Carolina utilities are planning on massive gas buildouts and are refusing to consider climate change in investment plans, as is its Indiana utility.

Southern Co. subsidiary Alabama Power, which acknowledged that it is not considering the parent company’s carbon goals in its integrated resource planning, is currently applying to the Alabama Public Service Commission for approval to spend over $1 billion to build and buy new gas-burning power plants.

Duke’s investments are particularly discordant with the earnings opportunity it could realize from a faster transition to clean energy, which Morgan Stanley characterized as the second largest of all utilities it assessed. The analysts said that approximately 90% of Duke’s coal fleet will become at risk of being undercut by lower-cost renewable energy by 2024.

The Morgan Stanley analysts dismissed concerns which some utilities have offered in the past about whether renewable energy would be sufficiently reliable, noting that “another important consideration, as renewables growth continues at a rapid rate, is reliability and resiliency of the grid, but we believe that we are far from reaching a level of renewables penetration that puts the system at risk.”

FirstEnergy has retirement opportunities in coal country

The analysts reported that none of FirstEnergy’s 3.4 GWs of regulated coal capacity is currently slated for retirement in the short or medium term, despite their estimation that all of that capacity will be rendered uneconomic by lower-cost wind energy by 2024.

While the analysts said that retiring that coal capacity offers “a meaningful earnings upside opportunity,” they said that retiring the coal plants that FirstEnergy owns in West Virginia might be difficult, given that state’s relationship to coal production.

If that’s the case, FirstEnergy would be missing out on earnings in part due to political flames that it has fanned over the years. Via its then-subsidiary FirstEnergy Solutions, a merchant generator which has since rebranded as Energy Harbor, FirstEnergy lobbied West Virginia officials aggressively for a bailout to its coal plant in 2019.

Morgan Stanley says Dominion’s ACP project will fail, freeing up money for renewables

The Morgan Stanley analysts said that they expected the Atlantic Coast Pipeline, co-owned by Dominion Energy and Duke, to fail, as first reported by Reuters in December.

But the analysts actually see that failure as a potential upside for Dominion’s stock, as it would free up capital to invest in renewable energy:

“We believe this project [the ACP] will not move forward due to legal risks, and believe that once this risk materializes D will pursue additional renewables investments,” the analysts wrote.

Writing in January, the analysts also said that state policy would be a key driver of Dominion’s transition from coal to clean energy. In March, the Commonwealth’s legislature passed the Virginia Clean Economy Act, which would require Dominion to power with 100% zero-carbon sources by 2045. The governor is expected to sign the bill. The legislation also will guarantee Dominion ownership rights to large amounts of offshore wind energy and may curtail regulators’ ability to oversee Dominion’s spending on wind energy.

APS can grow earnings by accelerating coal retirements beyond recent plans

Pinnacle West, the owner of APS in Arizona, announced in January that it would “eliminate fossil fuels” by 2050 and would retire its existing coal fleet by 2031.

The Morgan Stanley analysts suggested that APS could save customers money while increasing earnings if APS accelerates its coal retirement schedule even faster, estimating that all of APS’ coal capacity will be rendered uneconomic by low-cost solar by 2024.

The analysts said that they would evaluate whether APS is making good on the coal-to-clean opportunity based on what APS files in its integrated resource plan next month.

“We are incorporating this accretion in our bull case only despite the recent announcement of a faster than originally planned decarbonization as we need more evidence of the company’s ability to execute on greater capex and whether this is incremental to their current growth targets,” the analysts said.

APS has caused its regulatory relationship to deteriorate in recent years, the result of at least two electoral cycles of dark money and independent spending to influence the election of those regulators.

The company’s new CEO, Jeff Guldner, has pledged to cease all spending to influence regulators’ elections, but the worsened relationship caused by the drama of recent election cycles gave the analysts pause.

“The regulatory backdrop has become increasingly unpredictable,” they wrote.